Credit Card Calculator Payoff: Calculate Your Debt-Free Date

A few years ago, I checked my credit card statement and had the same thought many people do: "If I keep making the minimum payment, when will this balance actually disappear?" This is how a simple payoff calculator changed everything.

At first, I assumed it would take a couple of years. Then I used a credit card calculator payoff tool, and the results genuinely surprised me. The calculator showed that paying only the minimum would keep me in debt for much longer than I expected—and I'd pay a significant amount in interest along the way.

That moment completely changed how I looked at credit card debt.

Whether you're carrying a small balance or trying to eliminate thousands of dollars in debt, a credit card calculator payoff can help you understand where you stand and what changes will make the biggest difference.

What Is a Credit Card Calculator Payoff?

A credit card calculator payoff is an online tool that estimates:

- How long it will take to pay off your credit card

- The total interest you'll pay

- Your expected debt-free date

- How extra monthly payments affect your payoff timeline

Instead of guessing, you can see actual estimates based on your current balance, interest rate (APR), and monthly payment.

It's one of the easiest financial tools I've ever used because it turns confusing numbers into something you can actually understand.

Why I Started Using One

Like many people, I focused on one number: Minimum Payment Due.

Every month I paid exactly what the statement asked for.

I felt responsible because I never missed a payment.

The problem? I wasn't paying much toward the actual balance. Most of my payment went toward interest.

After entering my information into a payoff calculator, I realized that increasing my payment by just $75 per month could save me thousands of dollars in interest and help me become debt-free much sooner.

That small change completely changed my repayment plan.

How a Credit Card Calculator Payoff Works

Most calculators ask for only a few details.

1. Current Balance

This is the total amount you owe.

Example: $6,500

2. Annual Percentage Rate (APR)

Your APR determines how much interest your credit card charges.

Example: 19.99% APR

3. Monthly Payment

Enter either:

- Minimum payment

- Fixed monthly payment

- Percentage payment

4. Extra Monthly Payment (Optional)

Many calculators also allow you to add extra payments.

Even adding:

- $25

- $50

- $100

can make a noticeable difference over time.

Example Payoff Calculation

Let's look at a simple example.

Credit Card Balance: $8,000

APR: 22%

Monthly Payment: $220

Without paying anything extra, it may take several years to eliminate the balance, and you'll likely spend thousands of dollars on interest.

Now imagine increasing your monthly payment by just $100.

The calculator will often show:

- A much earlier payoff date

- Lower total interest

- Hundreds or even thousands of dollars saved

This is why I recommend using a calculator before deciding on your payment amount.

Benefits of Using a Credit Card Calculator Payoff

You Know Exactly What to Expect

Instead of wondering when you'll be debt-free, you'll have an estimated timeline. That makes budgeting much easier.

It Helps You Stay Motivated

Watching your payoff date move closer every time you increase your payment is surprisingly motivating. I found myself looking for small ways to save money just to make slightly larger payments.

You Can Compare Different Payment Amounts

One of my favorite features is experimenting with different numbers.

For example:

- What if I pay $50 extra?

- What if I pay $150 extra?

- What if I make two payments every month?

A calculator answers these questions in seconds.

It Helps You Understand Interest

Interest is easy to ignore because you don't always see it. A payoff calculator makes it visible. Once I saw how much interest I would pay over several years, paying extra every month became an easy decision.

Step-by-Step Guide to Using a Credit Card Calculator Payoff

Step 1: Check Your Latest Credit Card Statement

Write down:

- Current balance

- APR

- Minimum payment

Step 2: Open a Reliable Calculator

Choose a calculator that allows extra monthly payments and displays:

- Payoff schedule

- Interest paid

- Estimated payoff date

Step 3: Enter Your Numbers

Be accurate. Even small differences in APR or payment amount can affect the estimate.

Step 4: Test Different Payment Amounts

Try increasing your payment by:

- $25

- $50

- $100

- $200

See how much interest you save.

Step 5: Pick a Realistic Goal

Don't choose a payment amount that's impossible to maintain. Consistency matters more than making one large payment.

Calculate Your Payoff Plan Now

Enter your balance, APR, and monthly payment to see your exact debt-free date and how much you can save.

Try the Payoff Calculator →Small Changes That Make a Big Difference

After using a payoff calculator, I made a few simple adjustments.

Instead of ordering takeout three times a week, I reduced it to once a week. That saved around $80 every month. I added that money directly to my credit card payment. It didn't feel like a huge sacrifice, but over time it shortened my repayment schedule considerably.

Common Mistakes People Make

Paying Only the Minimum

Minimum payments keep your account in good standing, but they usually don't help you get out of debt quickly.

Ignoring the APR

Many people only look at their balance. The interest rate is just as important because it affects how much your debt costs over time.

Using the Credit Card Again

One mistake I made early on was paying down the balance and then using the card for new purchases. That slowed my progress. If possible, avoid adding new debt while paying off an existing balance.

Missing Payment Dates

Late payments can lead to late fees, higher interest rates, and credit score damage. Setting up automatic payments can help you avoid this.

Extra Tips That Worked for Me

These habits made repayment easier.

Round Up Every Payment

If your payment is $183, pay $200 instead. Those small amounts add up.

Use Unexpected Income

Whenever I received tax refunds, work bonuses, or cashback rewards, I put a portion toward my credit card. It helped reduce the balance much faster.

Pay More Than Once Per Month

Instead of making one payment, consider making two smaller payments during the month. This keeps your balance lower and may reduce interest, depending on how your card issuer calculates it.

Review Your Progress Monthly

Once a month, I updated my numbers in the calculator. Seeing my estimated payoff date move closer kept me motivated.

Who Should Use a Credit Card Calculator Payoff?

This tool is useful for almost anyone with credit card debt, including:

- College students managing their first credit card

- Families paying off multiple cards

- Professionals trying to reduce interest costs

- Anyone planning a debt-free budget

- People comparing different repayment strategies

Even if your balance is small, understanding your payoff timeline helps you make smarter financial decisions.

Frequently Asked Questions

Does paying extra every month really help?

Yes. Extra payments reduce your principal balance faster, which means less interest accumulates over time.

Can I pay off my credit card early?

In most cases, yes. Most credit card issuers don't charge a penalty for paying off your balance early.

Is a payoff calculator accurate?

A calculator provides an estimate based on the information you enter. Actual results may vary slightly due to changes in interest rates, fees, or future purchases.

Should I make one payment or multiple payments?

Both approaches work. Making multiple payments during the month can help keep your balance lower and make budgeting easier.

Final Thoughts

A credit card calculator payoff won't erase your debt overnight, but it gives you something just as valuable: clarity.

When I first used one, I realized that becoming debt-free wasn't about making dramatic changes. It was about understanding the numbers and making consistent, realistic payments every month.

If you haven't tried a payoff calculator yet, enter your current balance, APR, and monthly payment. Then test what happens when you add just $25 or $50 to your monthly payment. You may be surprised by how much interest you could save and how much sooner you could reach your goal of being debt-free.

Sometimes, seeing the numbers is all it takes to turn a plan into action.

Related Articles

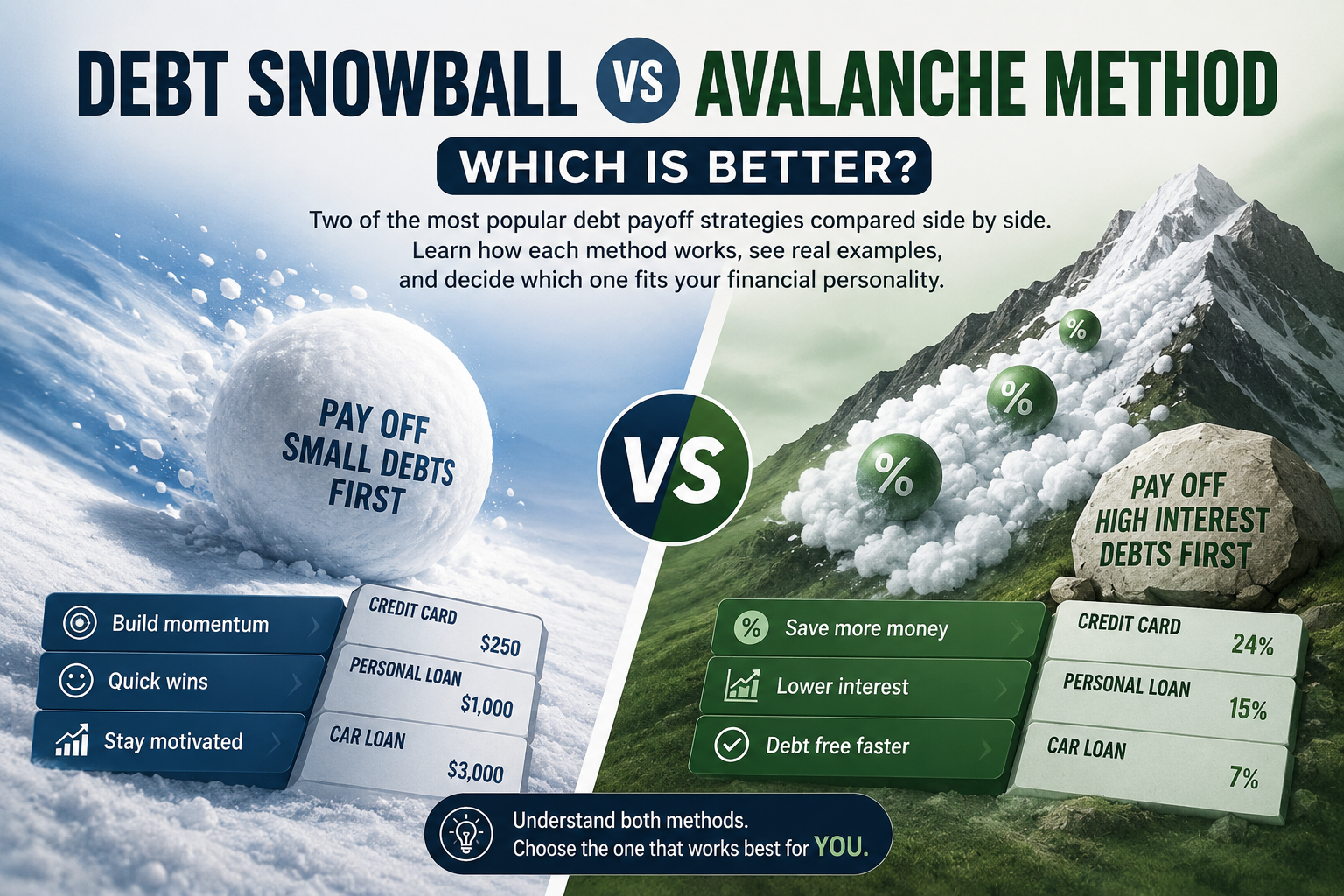

Debt Snowball vs Avalanche Method: Which Is Better?

Two of the most popular debt payoff strategies compared side by side. Learn how each method works and decide which one fits your financial personality.

How to Pay Off Credit Card Debt Fast

Discover proven strategies to eliminate your credit card debt quickly and save thousands in interest.