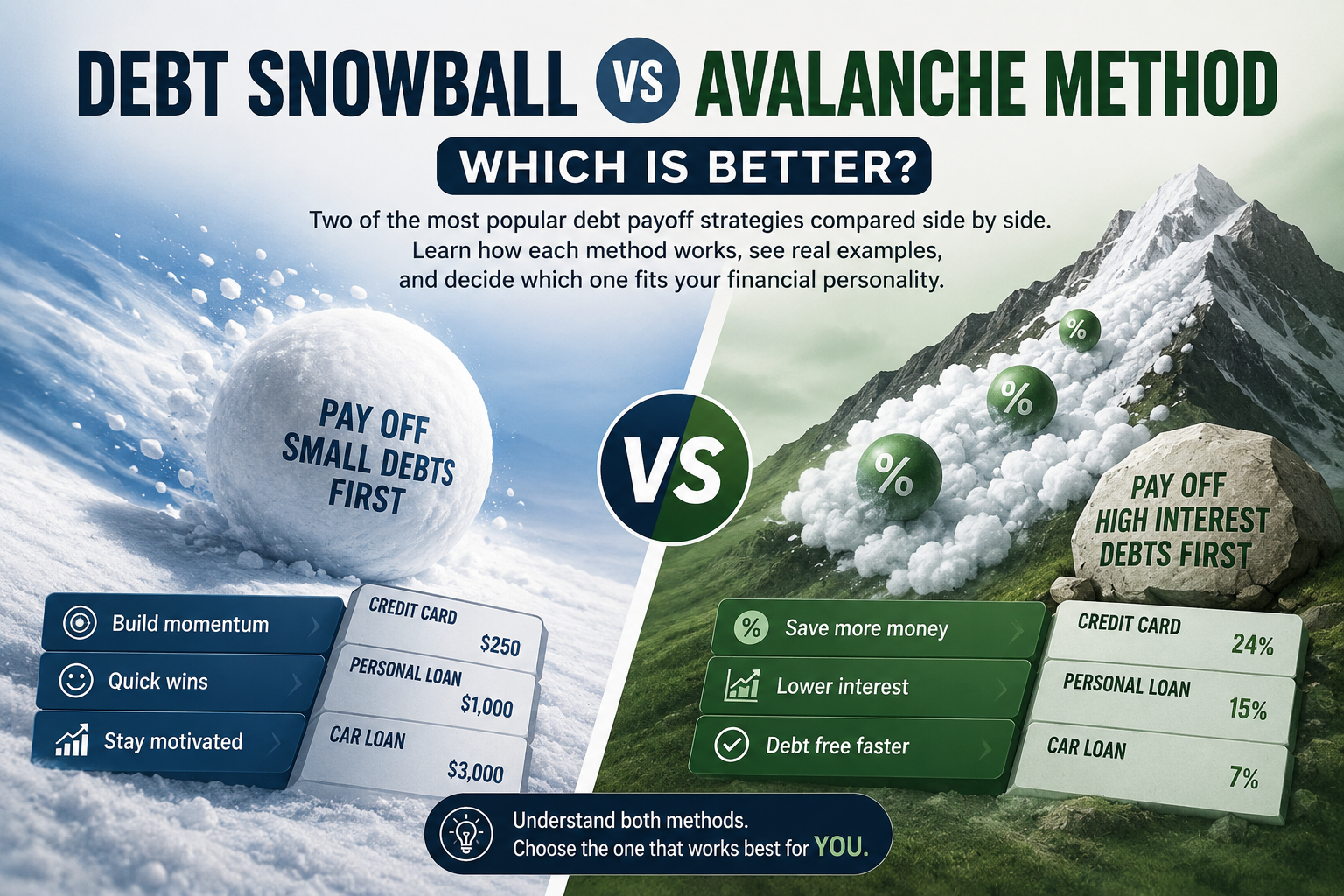

Debt Snowball vs Avalanche Method: Which Is Better?

Two of the most popular debt payoff strategies compared side by side. Learn how each method works, see real examples, and decide which one fits your financial personality.

Introduction: Choosing the Right Strategy

When it comes to paying off credit card debt, having a strategy is everything. Without a clear plan, it is easy to feel overwhelmed and make random payments that barely move the needle. The two most popular and widely recommended strategies are the debt snowball method and the debt avalanche method.

Both methods have helped millions of people become debt-free. But they work differently, and the best choice depends on your financial situation and personality. In this guide, we will break down exactly how each method works, compare them with real numbers, and help you pick the right one.

What Is the Debt Snowball Method?

The debt snowball method, popularized by personal finance expert Dave Ramsey, focuses on paying off your smallest debt first regardless of interest rate. Here is how it works:

- List all your debts from smallest balance to largest.

- Make minimum payments on all debts except the smallest one.

- Throw every extra dollar at the smallest debt until it is completely paid off.

- Once the smallest debt is gone, roll that payment into the next smallest debt.

- Repeat until all debts are paid off.

Why It Works

The snowball method is built on psychology, not math. Paying off small debts quickly gives you a sense of accomplishment and momentum. Each balance you eliminate feels like a win, which keeps you motivated to continue. For many people, this emotional boost is the difference between giving up and becoming debt-free.

What Is the Debt Avalanche Method?

The debt avalanche method takes a more mathematical approach. Instead of focusing on the smallest balance, you target the debt with the highest interest rate first. Here is the process:

- List all your debts from highest interest rate to lowest.

- Make minimum payments on all debts except the one with the highest APR.

- Put every extra dollar toward the highest-interest debt.

- Once that debt is gone, move to the next highest interest rate.

- Repeat until everything is paid off.

Why It Works

The avalanche method saves you the most money over time because you are attacking the most expensive debt first. By eliminating high-interest balances early, less of your money goes toward interest and more goes toward the principal. It is the mathematically optimal strategy.

Side-by-Side Comparison: A Real Example

Let us say you have three credit cards:

| Card | Balance | APR | Min. Payment |

|---|---|---|---|

| Card A | $1,200 | 15% | $30 |

| Card B | $4,500 | 22% | $100 |

| Card C | $2,800 | 18% | $60 |

Total debt: $8,500. Let us say you have $500 per month to put toward all your debts.

Snowball Order (Smallest to Largest)

Card A ($1,200) → Card C ($2,800) → Card B ($4,500)

With this approach, you payoff Card A in about 4 months, giving you an early win. Total estimated interest paid: approximately $1,950.

Avalanche Order (Highest APR First)

Card B (22% APR) → Card C (18% APR) → Card A (15% APR)

With this approach, you tackle the most expensive debt first. Total estimated interest paid: approximately $1,680.

The avalanche method saves about $270 in this example. However, with the snowball method, you get your first payoff win months earlier, which can be incredibly motivating.

Want to run your own numbers? Use our Credit Card Payoff Calculator to compare both scenarios with your actual balances.

See Your Personalized Payoff Plan

Enter your balances and see exactly how much time and money each method saves you.

Start Calculating Your Payoff Now →Which Method Should You Choose?

Here is a simple guide:

- Choose the Snowball if you need quick wins to stay motivated, have several small debts, or tend to lose focus on long-term goals.

- Choose the Avalanche if you are disciplined and numbers-driven, have a large high-interest debt, or want to save the maximum amount of money.

- Choose a Hybrid Approach if you want to start with one quick snowball win for motivation, then switch to the avalanche method for long-term savings.

5 Tips to Succeed With Either Method

- Stop using credit cards. You cannot fill a hole while you are still digging.

- Build a small emergency fund first. Even $500 prevents you from going back into debt for unexpected expenses.

- Automate your payments. Set up auto-pay for minimums so you never miss a due date.

- Track your progress. Use a spreadsheet, app, or our free calculator to visualize your declining balances.

- Celebrate milestones. Each card you payoff is a major achievement — acknowledge it!

Conclusion

Both the debt snowball and debt avalanche methods are proven strategies that work. The snowball gives you quick psychological wins; the avalanche saves you the most money. The best method is the one you will actually stick with.

No matter which strategy you choose, the key is to start today. Use our free Credit Card Payoff Calculator to model both strategies with your real numbers, and take the first step toward financial freedom.

For more strategies, read our complete guide on how to payoff credit card debt fast.

Frequently Asked Questions

What is the difference between snowball and avalanche?

The snowball method pays off the smallest balance first for quick wins. The avalanche method pays off the highest interest rate first to save the most money. Both require making minimum payments on all other debts.

Which method pays off debt faster?

The avalanche method typically pays off debt slightly faster because you save more on interest. However, the difference is often small. The snowball method can feel faster because you eliminate individual debts sooner.

Can I combine both methods?

Absolutely. A popular hybrid approach is to payoff one small debt first (snowball) for a quick confidence boost, then switch to the avalanche method for the remaining debts to maximize savings.

Does the snowball method cost more in interest?

Usually, yes — but the difference is often less than people expect. In many cases, it is a few hundred dollars. The psychological benefit of quick wins can be worth far more if it keeps you on track.

What is the debt payoff calculator and how can it help?

A credit card payoff calculator helps you model different payment scenarios. Enter your balance, APR, and monthly payment to see your exact payoff date, total interest, and potential savings from extra payments.