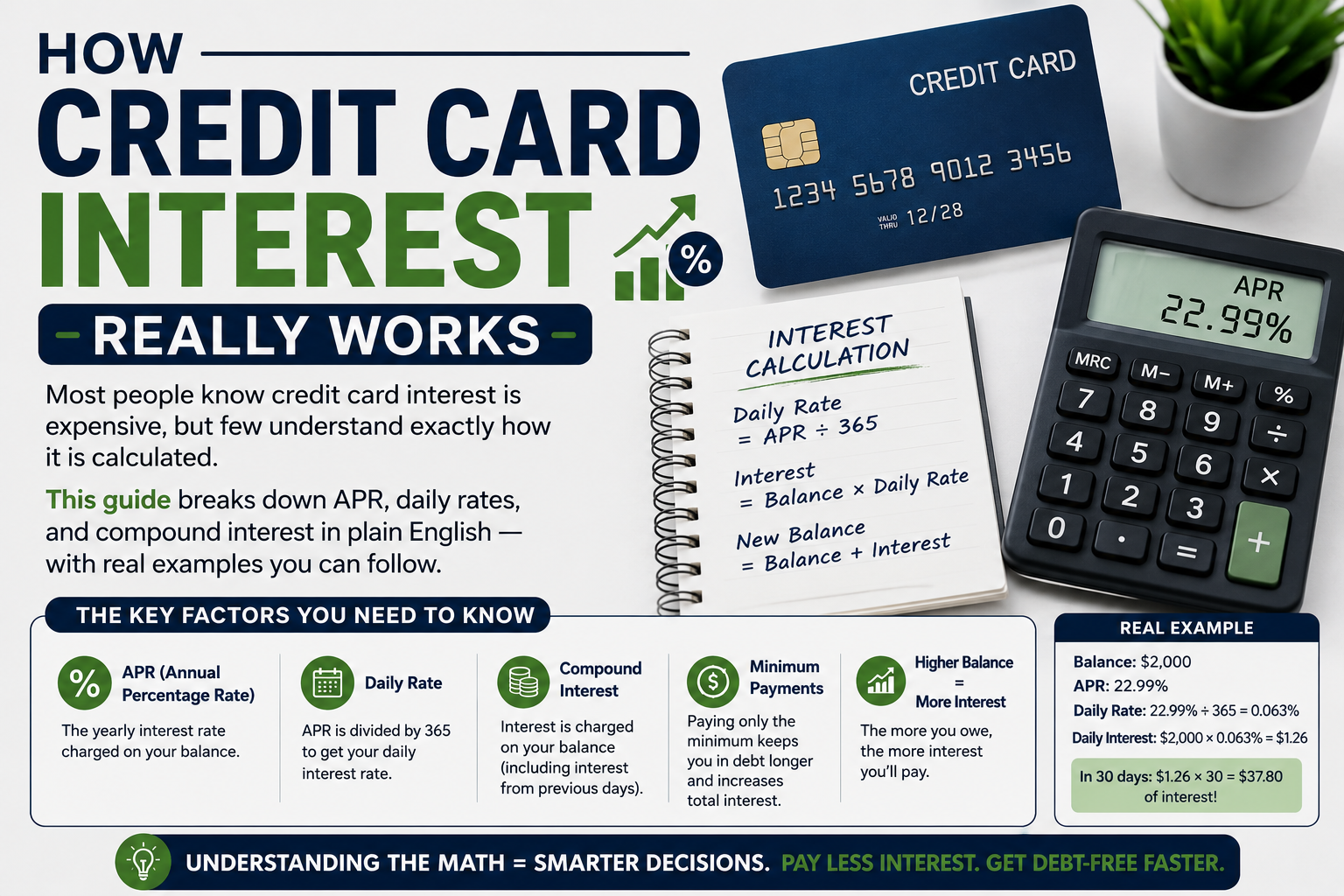

How Credit Card Interest Really Works

Most people know credit card interest is expensive, but few understand exactly how it is calculated. This guide breaks down APR, daily rates, and compound interest in plain English — with real examples you can follow.

Introduction: Why Understanding Interest Matters

Credit card interest is one of the most misunderstood concepts in personal finance. Many cardholders know they are paying interest, but they have no idea how much they are actually being charged or how the calculation works. This lack of understanding is exactly what costs people thousands of dollars every year.

When you understand how credit card interest really works, you can make smarter payment decisions, avoid costly mistakes, and payoff your debt significantly faster. Let us break it all down step by step.

What Is APR?

APR stands for Annual Percentage Rate. It is the yearly interest rate your credit card charges on any unpaid balance. For example, if your card has a 20% APR, that means you are being charged 20% interest on your balance over the course of a year.

But here is the important part: credit card interest is not charged once a year. It is calculated daily and compounded, which means it can add up much faster than most people expect.

Common APR Ranges

| Credit Score | Typical APR Range |

|---|---|

| Excellent (750+) | 14% – 18% |

| Good (700–749) | 18% – 22% |

| Fair (650–699) | 22% – 26% |

| Poor (below 650) | 26% – 30%+ |

How Is Credit Card Interest Calculated?

Credit card companies use a specific process to calculate your interest charges. Here is how it works in three steps:

Step 1: Find Your Daily Rate

Your daily rate (also called the daily periodic rate) is simply your APR divided by 365 days.

Daily Rate = APR ÷ 365

Example: 20% APR ÷ 365 = 0.0548% per day

Step 2: Calculate Your Average Daily Balance

Your credit card company looks at your balance every single day of the billing cycle (usually 28–31 days). They add up each day's balance and divide by the number of days in the cycle. This gives them your average daily balance.

For example, if you start the month with a $3,000 balance and make a $500 payment on day 15 of a 30-day cycle:

Days 1–14: $3,000 × 14 = $42,000

Days 15–30: $2,500 × 16 = $40,000

Average Daily Balance = ($42,000 + $40,000) ÷ 30 = $2,733.33

Step 3: Calculate the Monthly Interest Charge

Now multiply the average daily balance by the daily rate and by the number of days in the billing cycle:

Interest = Average Daily Balance × Daily Rate × Days in Cycle

$2,733.33 × 0.000548 × 30 = $44.93

So even after making a $500 payment, you are still charged nearly $45 in interest for that month. This is why understanding the math is so important.

The Power of Compound Interest (Working Against You)

Credit card interest compounds, which means you pay interest on your interest. If you do not payoff your full balance each month, the unpaid interest gets added to your principal balance. Next month, you are charged interest on the larger amount.

This is why a $5,000 balance at 20% APR with minimum payments can end up costing you more than $8,000 in total — you end up paying more in interest than the original amount you borrowed.

See How Much Interest You Are Really Paying

Enter your balance and APR to see your total interest cost and find out how much you can save.

Use Our Free Calculator Now →The Grace Period: How to Avoid Interest Entirely

Here is the good news: if you pay your full statement balance by the due date every month, most credit cards will not charge you any interest at all. This is called the grace period, and it typically lasts 21–25 days after your billing cycle closes.

The grace period only applies when you pay in full. If you carry any balance from the previous month, the grace period usually disappears, and interest starts accruing on all new purchases immediately.

Why Minimum Payments Are a Trap

Credit card companies set minimum payments intentionally low — usually 1–3% of your balance or a fixed amount like $25, whichever is greater. This keeps you in debt as long as possible.

Example: The True Cost of Minimum Payments

Let us say you have a $6,000 balance at 22% APR with a $120 minimum payment:

- Time to payoff: Approximately 9 years

- Total interest paid: Over $6,800

- Total amount paid: Nearly $12,800 for a $6,000 debt

Now, if you increase your payment to just $250 per month:

- Time to payoff: About 31 months

- Total interest paid: Approximately $1,750

- You save: Over $5,000 in interest and 6+ years of payments

Use our Credit Card Payoff Calculator to see your exact savings with different payment amounts.

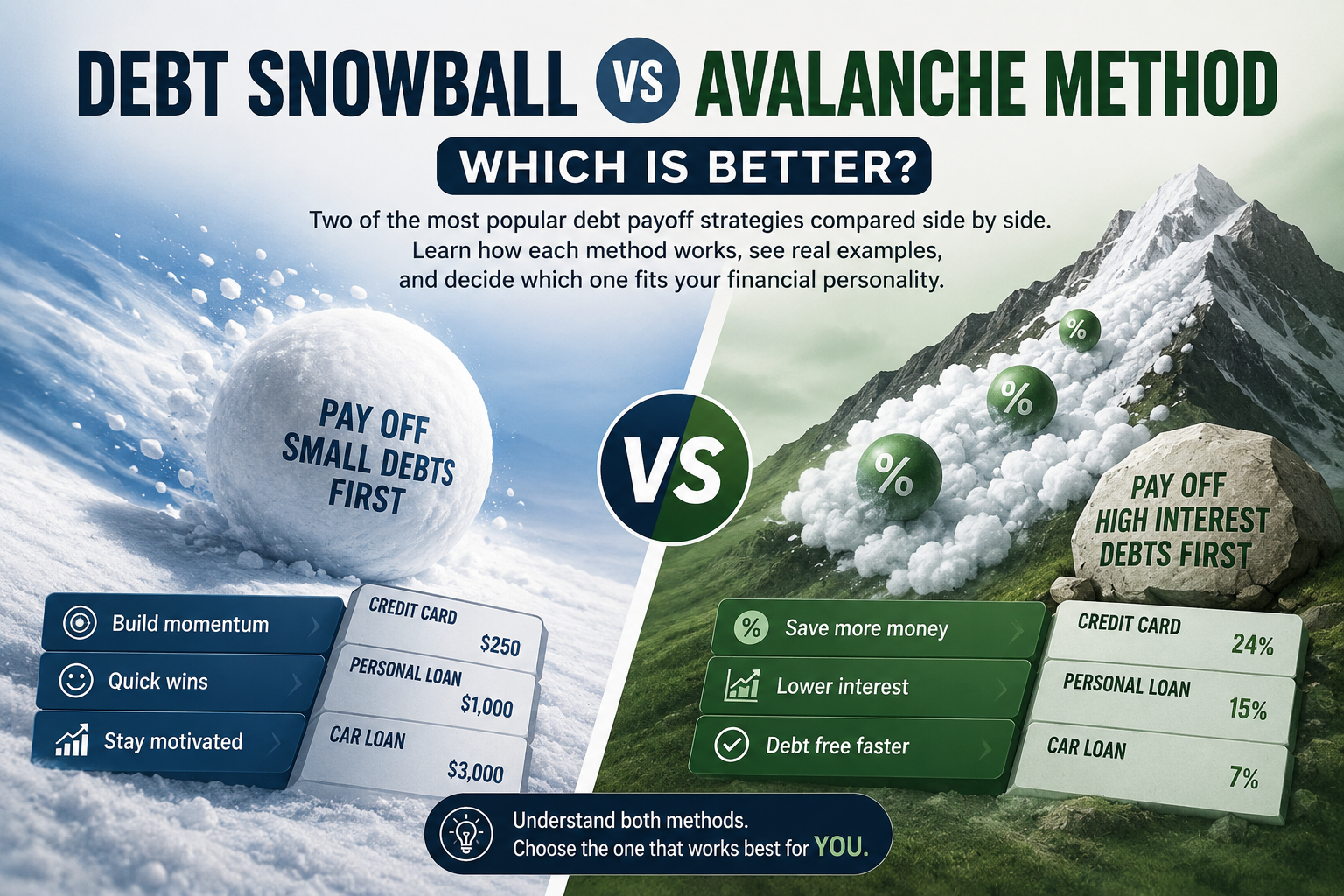

5 Ways to Reduce Your Credit Card Interest

- Pay your full balance every month. This eliminates interest charges completely.

- Pay more than the minimum. Even $50 extra per month makes a significant difference over time.

- Call and negotiate a lower rate. If you have a good payment history, many issuers will reduce your APR.

- Consider a balance transfer. A 0% introductory APR card can save you hundreds while you pay down the principal. Learn more about payoff strategies in our guide to paying off credit card debt fast.

- Use a debt payoff strategy. The snowball or avalanche method gives you a clear, focused plan to eliminate debt efficiently.

Conclusion

Credit card interest is designed to be confusing, but it does not have to be. Now you know how APR converts to a daily rate, how your average daily balance is calculated, and why compound interest can make even a moderate balance incredibly expensive over time.

The most powerful thing you can do is pay more than the minimum every month. Even small increases in your payment can save you thousands of dollars and years of stress. Use our free Credit Card Payoff Calculator to see exactly how much you can save — it takes less than 30 seconds.

Frequently Asked Questions

What does APR mean on a credit card?

APR stands for Annual Percentage Rate. It represents the yearly cost of borrowing on your credit card. A 20% APR means you will pay 20% of your outstanding balance in interest charges over one year if you carry a balance.

Is credit card interest charged monthly or daily?

Credit card interest is calculated daily using your daily periodic rate (APR ÷ 365). However, the resulting interest charges appear on your monthly statement. The daily calculation means interest compounds more aggressively than many people realize.

How can I avoid paying credit card interest?

Pay your full statement balance by the due date every month. This takes advantage of the grace period, and you will never be charged interest. If you cannot pay in full, pay as much as possible above the minimum to minimize interest charges.

Why is my interest charge different every month?

Your interest charge varies because it is based on your average daily balance, which changes depending on when you make purchases and payments during each billing cycle. A credit card interest calculator can help you estimate your charges.

Does paying twice a month reduce interest?

Yes! Making payments twice a month (or more frequently) lowers your average daily balance, which directly reduces the interest charged. For example, paying $250 on the 1st and $250 on the 15th costs you less in interest than paying $500 once at the end of the month.