How to PayOff Credit Card Debt Fast

Struggling with credit card balances? Discover proven strategies, real-world examples, and actionable tips to eliminate your debt faster than you ever thought possible.

Introduction: The Credit Card Debt Trap

Credit card debt is one of the most stressful financial burdens millions of people face every day. If you are carrying a balance from month to month, you know the feeling — watching interest charges pile up while your minimum payments barely make a dent. The good news is that you are not stuck. With the right approach, you can payoff credit card debt fast and save yourself thousands of dollars in the process.

In this guide, we will walk you through proven strategies that real people use to become debt-free. Whether you owe $2,000 or $20,000, these tips will help you build a clear plan and stick to it.

1. Know Exactly What You Owe

The first step to paying off credit card debt is to face the numbers. Many people avoid looking at their total balance because it feels overwhelming. But you cannot fix a problem you do not fully understand.

Start by listing every credit card you have, along with:

- The current balance on each card

- The annual percentage rate (APR) for each card

- The minimum monthly payment required

Once you have everything written down, you can see the full picture. This is your starting point, and it is an essential step that most people skip.

2. Stop Adding New Charges

This sounds simple, but it is the most important rule: stop using your credit cards while you are paying them off. Every new charge adds to your balance and undoes your progress. Consider switching to cash or a debit card for daily expenses.

If you rely on credit cards for emergencies, set aside even a small emergency fund — $500 to $1,000 — so you do not have to reach for plastic when something unexpected happens.

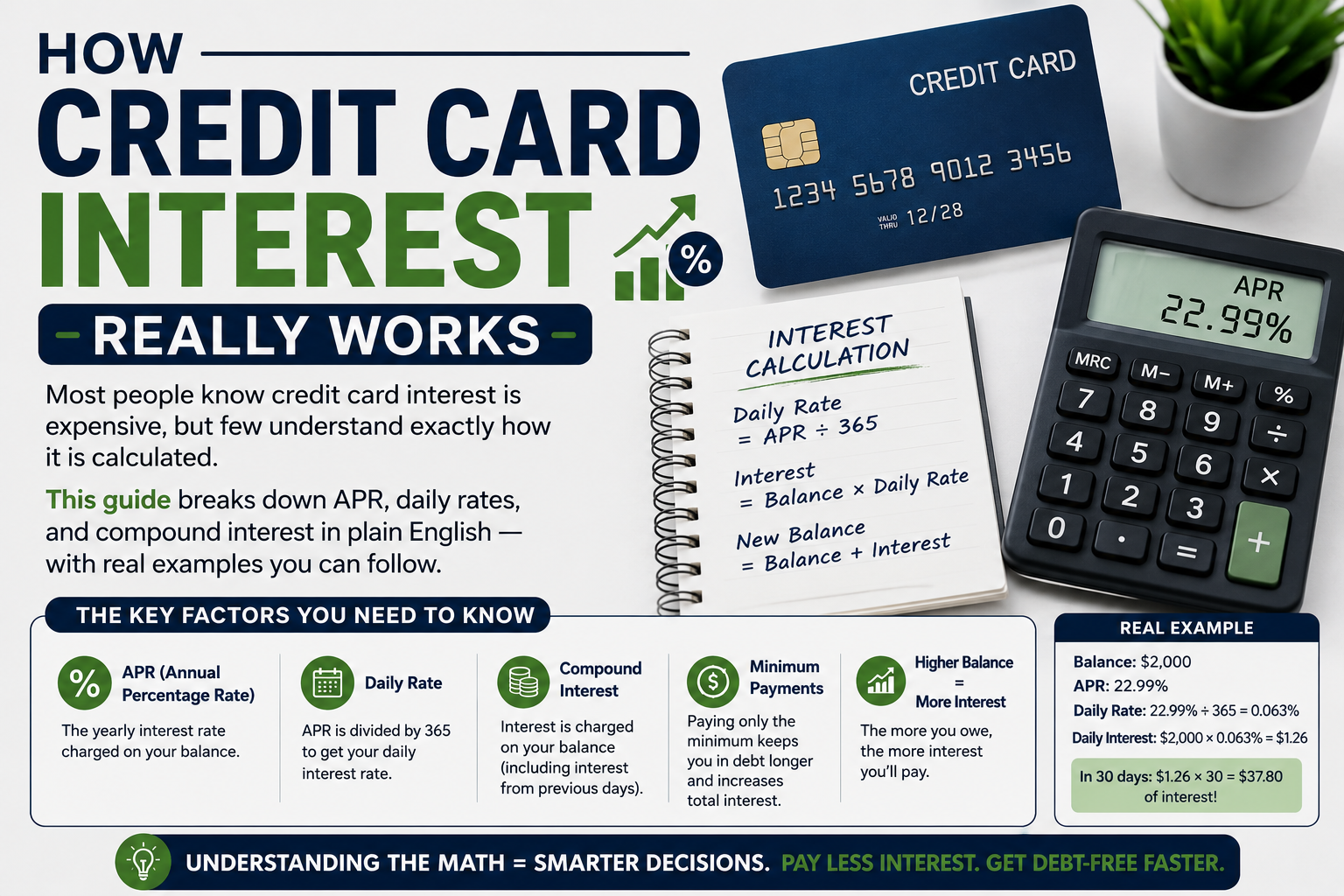

3. Pay More Than the Minimum

Minimum payments are designed to keep you in debt as long as possible. On a $5,000 balance at 20% APR, paying only the minimum could take over 20 years and cost you more than $8,000 in interest alone.

Even adding $50 or $100 extra per month can cut years off your payoff timeline. Use our Credit Card Payoff Calculator to see exactly how much time and money you can save by increasing your payments.

Real Example

Let us say you have a $7,000 balance at 22% APR with a $200 monthly payment. Without extra payments, it takes about 55 months and costs $3,900 in interest. But if you add just $100 extra per month ($300 total), you pay it off in 30 months and save over $1,800 in interest. That is the power of paying more than the minimum.

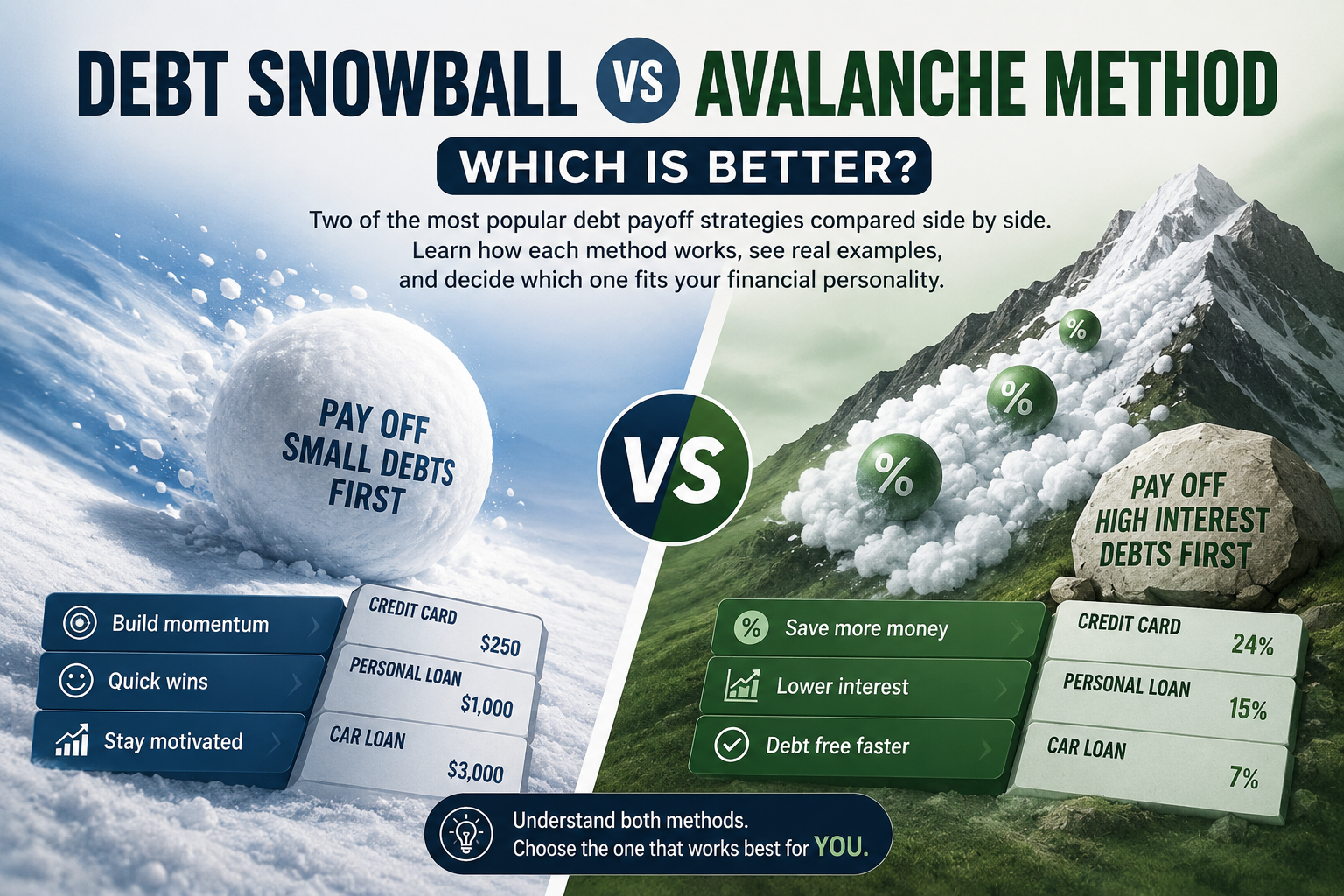

4. Choose a Debt Payoff Strategy

Two of the most popular methods are the debt snowball and the debt avalanche. Both work — they just approach the problem differently.

- Debt Snowball: Payoff your smallest balance first. The quick wins keep you motivated.

- Debt Avalanche: Payoff the card with the highest interest rate first. This saves you the most money mathematically.

Not sure which one is right for you? Read our detailed comparison: Debt Snowball vs Avalanche Method.

5. Negotiate a Lower Interest Rate

Many people do not realize that you can call your credit card company and ask for a lower interest rate. If you have been a good customer with a history of on-time payments, there is a decent chance they will agree. Even a 2–3% reduction can save you hundreds of dollars over the life of your debt.

Here is a simple script you can use: "Hi, I have been a loyal customer for [X years] and I am working on paying down my balance. I was wondering if you could lower my interest rate to help me pay it off faster."

6. Consider a Balance Transfer

If you have good credit, a balance transfer card with a 0% introductory APR can give you breathing room. This lets you pay down the principal without interest for 12–21 months. Just watch out for balance transfer fees (usually 3–5%) and make sure you have a plan to payoff the balance before the promotional period ends.

7. Find Extra Money in Your Budget

Look for areas where you can temporarily cut back and redirect that money toward your debt. Common areas include:

- Dining out and takeout

- Streaming subscriptions you rarely use

- Impulse purchases

- Gym memberships (try home workouts temporarily)

Even small savings add up. Redirecting just $5 per day toward your credit card is $150 per month — that could cut years off your debt.

8. Increase Your Income

If cutting expenses is not enough, consider ways to earn more. Side gigs like freelancing, tutoring, driving for a rideshare service, or selling items you no longer need can all generate extra cash. Every extra dollar you throw at your credit card debt accelerates your payoff date.

Ready to See Your Payoff Plan?

Enter your balance, interest rate, and payment amount to get a personalized payoff timeline in seconds.

Start Calculating Your Payoff Now →9. Automate Your Payments

Set up automatic payments for at least the minimum amount on all your cards. This ensures you never miss a payment and avoid late fees. Then manually add extra payments whenever you have additional funds. Consistency is the key to paying off debt fast.

10. Track Your Progress and Stay Motivated

Paying off debt is a marathon, not a sprint. Track your progress monthly. Celebrate milestones — paying off your first card, hitting the halfway point, making your final payment. Visual progress keeps you motivated during the tough months.

Conclusion

Paying off credit card debt fast is absolutely possible, but it requires a plan and commitment. Start by understanding what you owe, choose a payoff strategy, and find ways to pay more than the minimum every month. Small, consistent actions lead to massive results over time.

The most important step is the first one. Use our free Credit Card Payoff Calculator right now to see your personalized payoff date and start your journey toward financial freedom today.

Frequently Asked Questions

How long does it take to payoff credit card debt?

It depends on your balance, interest rate, and monthly payment. A $5,000 balance at 20% APR with $200 monthly payments takes about 32 months. Adding extra payments can significantly reduce this timeline.

Is it better to payoff one card at a time or all at once?

It is generally more effective to focus on one card at a time while making minimum payments on the others. This is the core idea behind both the snowball and avalanche methods.

Should I use my savings to payoff credit card debt?

Keep a small emergency fund ($500–$1,000), then use any extra savings to pay down high-interest debt. Credit card interest rates are usually much higher than savings account returns, so paying off debt is often the smarter financial move.

Can I negotiate my credit card debt?

Yes. You can negotiate a lower interest rate, and in some cases of financial hardship, credit card companies may offer a settlement for less than the full amount owed. Always communicate with your card issuer if you are struggling.

What is the fastest way to payoff $10,000 in credit card debt?

Combine strategies: use the avalanche method, negotiate lower rates, cut expenses aggressively, and increase your income. With a $500 monthly payment on a 20% APR card, you can payoff $10,000 in about 24 months. Try our calculator to see your exact timeline.